Thinking of Closing That Car Loan Early? Whether you’re facing a financial crunch or just want to free yourself from those monthly EMIs, understanding the car loan settlement process is essential.

Most people don’t realize how things like loan foreclosure, settlement offers, or even prepayment penalties can affect their credit score and future borrowing capacity.

In this guide, you’ll get a no-jargon, complete walkthrough of how to settle your car loan in India the smart way—without getting burned.

Why You Must Understand Car Loan Settlement

You’ve paid your EMIs for years, but life happens—or you suddenly have a lump sum. Whether you’re declaring financial crisis or just ready to own your ride outright, knowing the car loan settlement process matters.

Lenders may offer loan settlement, but it affects your credit score, triggers prepayment charges, and requires paperwork like a No Dues Certificate (NDC). This guide breaks down everything you need to know in simple steps.

1. What Is Car Loan Settlement?

Car loan settlement (also called loan foreclosure or one‑time settlement) means paying off the outstanding loan amount—often less than full dues—as a lump sum to close the account. The lender may waive the rest and mark the loan as settled on your credit report.

But beware: a “settled” status is not the same as “closed.” Settled = red flag to lenders. It stays on your credit report and can hurt your chances of getting future loans.

Book a Paid Consultation

Got questions about your loan situation? Chat directly with our Helpdesk on WhatsApp to book a consultation with Mr Sharma and get clarity on your next step. No middlemen. No judgment. Just real help.

Contact Helpdesk2. Prepayment vs Settlement: Know the Difference

| Option | What You Do | Charges | Credit Impact |

|---|---|---|---|

| Full Prepayment | Lump‑sum full remaining amount | May incur 2–5% penalty | Clean, marked “Closed” |

| Part Prepayment | Pay partial principal early | ~3% part-payment fees | Clean, tenure/EMI reduced |

| Loan Settlement | Negotiate reduced settlement amount | May include waiver | Negative: marked “Settled” |

Example:

Let’s say you still owe ₹2.5 lakhs on your car loan. You negotiate a one-time settlement at ₹1.8 lakhs. The bank accepts. Your EMI stops—but your credit report will show this loan as “settled,” not “closed.”

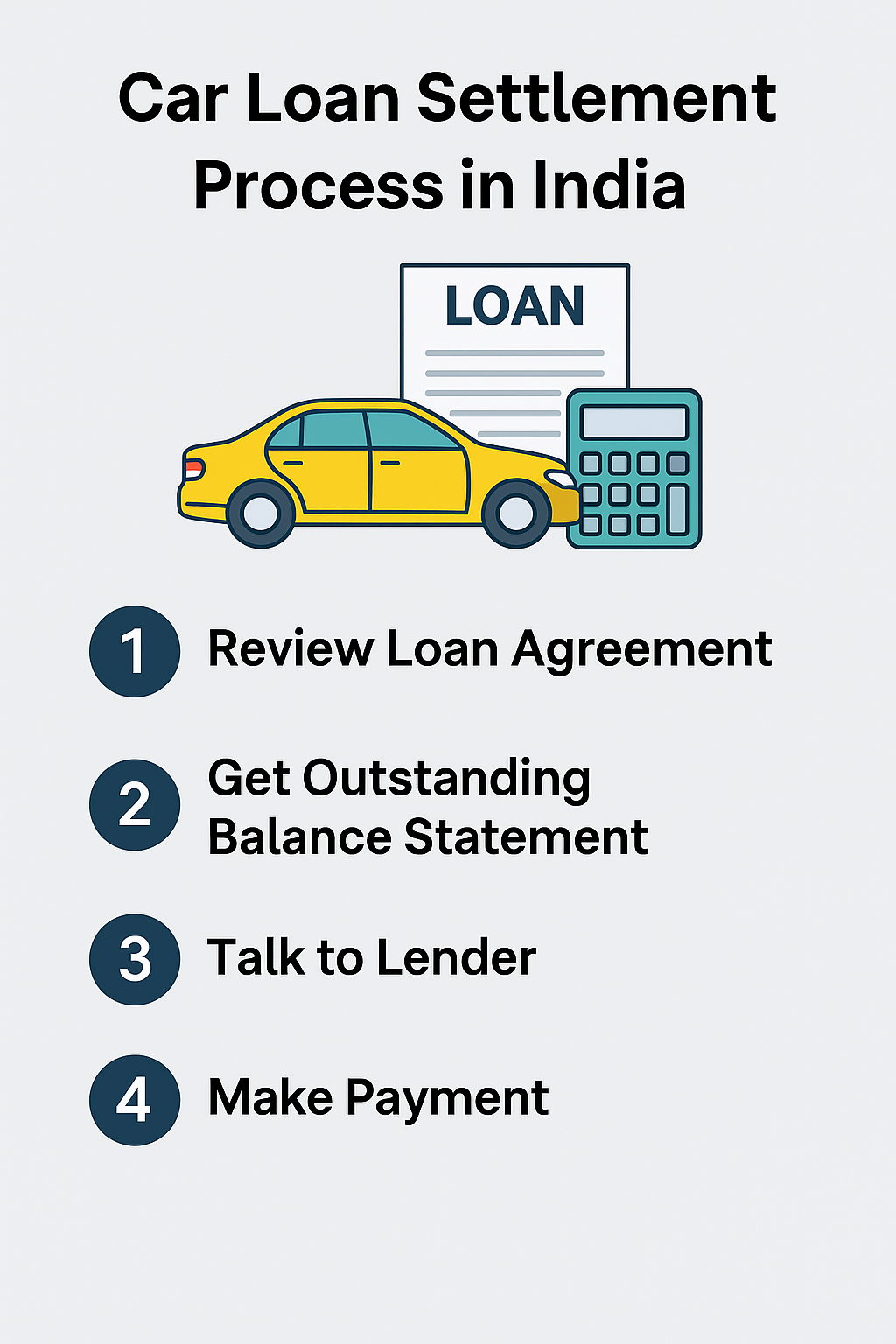

3. Step-by-Step: How to Settle or Foreclose Your Car Loan

Step 1: Review Your Loan Agreement

Go through your original loan agreement and note:

- Prepayment and foreclosure clauses

- Lock-in periods (typically 6–12 months)

- Penalty percentages and conditions

Step 2: Get Outstanding Balance Statement

Request your latest loan balance statement. This will include:

- Pending principal

- Interest due

- Prepayment or foreclosure charges

Step 3: Talk to Your Lender

Reach out to your bank/NBFC to:

- Inquire about prepayment and settlement options

- Check if you qualify for reduced settlement due to financial hardship

- Ask for a formal quote in writing

Step 4: Make the Payment

Once agreed:

- Pay the negotiated or full closure amount

- Use a traceable payment method like RTGS, cheque, or bank transfer

Step 5: Collect All Closure Documents

After payment, immediately collect:

- No Dues Certificate (NDC)

- Loan closure letter

- RC release letter for hypothecation removal

Step 6: Verify With Credit Bureaus

In 30–45 days:

- Check your CIBIL/Equifax report

- Make sure the loan status is updated correctly (Closed or Settled)

4. Impact on Credit Score & Future Borrowing

Loan settlement can lower your credit score by 75–100 points or more. It stays on your credit report for up to 7 years.

Even though you’re done paying, lenders view a “settled” loan as a risk. That means:

- Higher interest rates on future loans

- Possible rejection for big loans like home or business loans

- Lower credit card limits

To avoid this, choose foreclosure or full prepayment if possible.

5. When Should You Opt for Loan Settlement?

You should consider loan settlement only when:

- You’ve already defaulted on EMIs

- You’re in a genuine financial crisis

- You can’t restructure or refinance your loan

Avoid settlement if:

- You have the means to foreclose

- You’re close to completing the loan tenure

- You want to preserve your credit health

6. What Banks Typically Charge for Prepayment in India

Typical Prepayment Charges by Indian Banks:

- ICICI Bank: 3% if prepaid within 12 months, 2% from 13–24 months, zero after

- Axis Bank: ~2–3% prepayment charge if <24 EMIs paid

- HDFC, SBI, Kotak: Similar structures—lower charges after 1–2 years

Pro Tip: Try to prepay after 24 months to avoid extra charges.

9. Final Checklist Before Closing Your Car Loan

✅ Review loan agreement

✅ Get written settlement or foreclosure quote

✅ Pay via secure channel

✅ Collect NDC and closure documents

✅ Remove hypothecation from RC

✅ Confirm loan closure on credit report

✅ Keep physical and digital proof

Suggested reading: Personal loan settlement process in 2026

Bottom-Line: Choose Wisely

✔ If you can prepay in full, do it—it’s the cleanest way to close your loan

✔ If you’re struggling financially, a settlement may be necessary—but it will dent your credit

✔ If you’re midway, explore restructuring or EMI adjustments first

✔ Don’t settle out of laziness. Understand your rights, negotiate hard, and walk away with documents in hand

Done right, closing your car loan can save you stress, money, and future trouble. So be smart, be timely—and never skip the NOC.

Who is Mr. Sharma

Mr. Sharma is the founder and lead consultant at Sharma Debt Solutions™ — a result-driven advisor with years of hands-on experience helping borrowers navigate personal loan defaults, credit card debt, and recovery agent pressure.

His journey began not in courtrooms, but in the real struggles of everyday people. With deep practical knowledge and an independent network of legal professionals across the country, Mr. Sharma has helped loan defaulters regain peace of mind through strategic guidance and smart action.

He personally oversees each case, ensuring clients are not just heard — but empowered. Whether you’re seeking clarity on your next step or a trusted hand to walk you through the process, Mr. Sharma brings unmatched dedication and insight to every consultation.

“It’s not just about solving debt — it’s about restoring confidence, control, and dignity.”