Let’s face it — no one plans to default on a loan. When life hits hard, people settle debts just to breathe again.

But when things calm down, a new fear creeps in: “Can I ever get another loan after settlement?”

If that’s your question, here’s the real answer:

Yes, you can get a loan after settlement — but only if you rebuild your credit systematically.

In India, lenders don’t blacklist you forever. They just need proof that the financial chaos is behind you.

This article gives you that roadmap — clear, practical, and designed for the Indian credit system.

If you’re still unclear about how settlements work, read our full guide on Loan Settlement Agency in India — it explains how professionals handle negotiations and legal closures before you begin your rebuild.

What “Settlement” Really Means (and Why It Matters)

When you settle a loan, it means the bank agreed to accept a partial payment to close the account — less than what you actually owed.

It happens after the account turns NPA (Non-Performing Asset), and recovery looks difficult.

On your CIBIL report, it doesn’t show as Closed — it shows as:

Status: Settled

That single word creates a chain reaction.

To the next lender, it means:

“This borrower couldn’t pay the full amount once — may happen again.”

So even if you’ve cleared the case emotionally, your credit report keeps the memory — for up to 7 years.

Can I Get Loan After Settlement?

Yes — but not immediately, and not without rebuilding your reputation.

Think of it this way:

The bank didn’t “ban” you. It just moved you to a higher-risk category.

You can move back to “normal” by proving that your financial discipline has returned.

How long it takes depends on:

- How recent your settlement was

- How low your CIBIL score dropped

- How clean your record is now

- The type of loan you’re applying for

Impact of Settlement on Your Credit Report

A “settled” remark affects three key areas:

| Factor | Impact | Recovery Time |

|---|---|---|

| CIBIL Score | Drops by 75–150 points | 12–24 months |

| Lender Trust | Immediate loss; viewed as high-risk | 18–30 months |

| Loan Eligibility | Limited to secured loans only | 12–36 months |

If your score has fallen below 650, expect stricter checks, smaller limits, or rejections for unsecured products.

How Long Does It Take to Get a Loan After Settlement?

Here’s the realistic timeline:

| Time Since Settlement | Loan Eligibility | What You Should Focus On |

|---|---|---|

| 0–6 months | ❌ Very low | Fix errors, collect documents |

| 6–12 months | ⚠️ Low | Start secured credit card / small FD loan |

| 12–24 months | ✅ Moderate | Maintain perfect record, apply strategically |

| 24+ months | ✅✅ Good | Apply for mainstream credit with confidence |

Which Loans Are Easier to Get After Settlement?

Not all loans have equal resistance. Here’s your realistic approval hierarchy:

| Loan Type | Probability | Why |

|---|---|---|

| FD-backed Credit Card | High | Minimal risk to bank |

| Gold Loan / Loan Against Asset | High | Collateral covers default risk |

| Two-Wheeler Loan | Moderate | Some banks lenient with steady income |

| Used Car Loan (with Co-applicant) | Moderate | Joint responsibility lowers risk |

| Personal Loan (Unsecured) | Low | Hard until 18–24 months of clean record |

| Home Loan | Moderate after 24 months | Collateral + co-applicant improves chance |

| Business Loan (Secured) | Moderate-High | Depends on cash flow documentation |

In short: secured loans first, unsecured later.

Why Lenders Hesitate — The Risk Lens

When you apply for a fresh loan after settlement, lenders run your credit history through risk scoring models.

They’re not emotional — they’re algorithmic.

The system checks:

- Missed EMI patterns

- “Settled” tags

- Number of credit inquiries

- Active delinquencies

- Utilization ratio

If your file shows frequent applications or multiple defaults, you’re flagged as “high-risk.”

That’s why patience and spacing out applications matter more than enthusiasm.

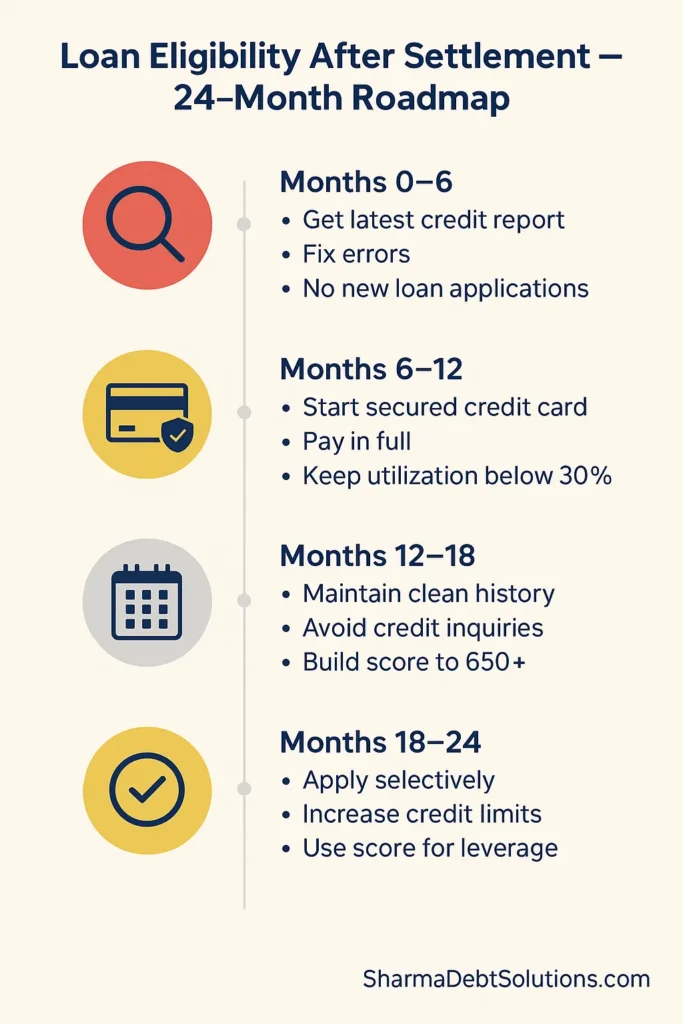

The 24-Month Credit Rebuild Plan (Step-by-Step)

Months 0–3 — Clean Up the Past

- Get your latest CIBIL / Experian report.

- Check for any reporting errors (like active overdue on settled loan).

- Collect and scan your settlement letter and NOC — keep forever.

- Do not apply for new loans. Every rejection worsens your profile.

Months 3–6 — Re-enter with Collateral

- Open a secured credit card against a fixed deposit (₹10k–₹25k).

- Use it lightly (₹2k–₹5k monthly) and pay in full every cycle.

- Keep utilization below 30% of limit.

- Optional: take a small gold loan or FD-backed loan and repay diligently.

Months 6–12 — Build a Payment History

- Continue your secured card usage.

- Maintain zero missed payments — even one delay restarts your timeline.

- Avoid payday or quick-cash apps. They hurt more than help.

- Track your score quarterly — small increases show you’re on the right path.

Months 12–18 — Gradual Expansion

- Apply for a small personal loan only if your score has crossed 650.

- Choose lenders who do manual underwriting (IDFC First, RBL, Bajaj Finance, etc.).

- Consider a co-applicant if possible — reduces perceived risk.

- Keep older credit lines active and well-managed.

Months 18–24 — Return to Mainstream

- You’re now ready for standard loans: credit cards, personal loans, even home loans.

- Request limit enhancements on existing cards instead of new ones.

- Use your improved score as leverage for better interest rates.

How to Increase Your Loan Approval Odds

- Maintain clean salary credits and steady job history.

- Keep utilization ratio <30%.

- Avoid new credit cards right before applying for a major loan.

- Keep only 1–2 active loans — more signals instability.

- Offer collateral whenever possible.

- Use co-applicant or guarantor for better terms.

Every small sign of reliability pushes your application from risk to consider.

Removing or Improving the “Settled” Remark

You can’t erase a genuine settlement, but you can improve it.

Here’s how:

- Pay the remaining balance (if affordable).

- Request bank to mark status as Closed / Paid in Full.

- Obtain a written confirmation from the lender.

- Raise a CIBIL dispute to update the record.

- Wait 30–45 days for the new entry to reflect.

This method can boost your score by 50–80 points instantly if processed properly.

For official reference, see the RBI’s Framework for Compromise Settlements and Technical Write-offs (June 2023) .

Example: Real Recovery Stories

Case 1 — The Salaried Comeback

- Settled ₹2.5 lakh personal loan in 2022.

- Took FD-backed card, paid in full every month.

- After 15 months, CIBIL: 560 → 715.

- Approved for ₹6 lakh used car loan with co-applicant.

Case 2 — The Business Bounce-Back

- Defaulted during COVID. Settled ₹5 lakh business loan.

- Took small equipment loan with collateral, paid on time for 20 months.

- Secured ₹10 lakh business top-up in 2024 at 12% interest.

Case 3 — The Long Rebuilder

- Two settlements (credit card + personal loan).

- 30 months of clean repayment + FD-card.

- CIBIL improved from 510 → 698. Now holds standard credit card and EMI card.

Common Mistakes to Avoid

- Paying agents who claim to “delete settled accounts.”

- Applying to 10 lenders at once — instant red flag.

- Missing small credit card payments (they count too).

- Letting your secured card lapse.

- Ignoring your settlement NOC — it’s legal proof forever.

Documents You’ll Need for Future Loan Applications

| Category | Examples |

|---|---|

| Identity Proof | PAN, Aadhaar |

| Income Proof | Salary slips, ITR, bank statements (12 months) |

| Settlement Proof | Letter + NOC from lender |

| Credit Report | CIBIL / Experian (latest) |

| Collateral Docs (if secured loan) | FD receipt, gold valuation, property papers |

Keeping these ready shows professionalism and transparency.

Sample Message to a Relationship Manager

“Dear Sir/Madam, I had settled a loan with [Bank Name] in [Month Year]. My credit report is now updated. I have maintained clean repayments for over a year and would like to explore new loan options. Kindly guide me regarding eligibility and required documents.”

Short, confident, and factual — not apologetic.

India-Specific Credit Improvement Tactics

- Use CIBIL-linked secured credit cards (HDFC, IDFC, SBI).

- Monitor your score quarterly through Paisabazaar or CRED (free).

- Maintain at least 12 EMIs with zero delays — CIBIL rewards consistency.

- Pay off any small residual dues; even ₹200 pending can keep a default tag alive.

- Ensure your mobile number and email are consistent across banks — it helps match data faster.

Loan After Settlement: Probabilities by Product

| Product | Typical Score Needed | Chance After 1 Year | Chance After 2 Years |

|---|---|---|---|

| Gold Loan | 550+ | ✅ High | ✅✅ Very High |

| FD-backed Card | Any | ✅ High | ✅✅ Very High |

| Two-Wheeler Loan | 620+ | ⚠️ Moderate | ✅ High |

| Used Car Loan | 640+ | ⚠️ Moderate | ✅ High |

| Personal Loan (Unsecured) | 680+ | ❌ Low | ✅ Moderate |

| Home Loan | 700+ | ⚠️ Low | ✅ High |

Pro Tip — Timing Matters

Apply for new loans only after 15–20 days of your CIBIL score update.

Fresh updates improve your rating snapshot and boost approval odds.

When Should You Consider Paying Off the Settled Balance?

If you’re aiming for:

- Home loan within 2 years, or

- Business credit line,

then it’s worth paying the leftover settlement difference.

Because premium lenders (like SBI, HDFC, Axis) prefer “Closed” status over “Settled.”

Otherwise, continue rebuilding — time heals your CIBIL naturally.

Frequently Asked Questions

1. How soon after settlement can I get a loan?

Usually 12–24 months, depending on credit rebuild speed. Secured loans possible earlier.

2. Will banks see my old settlement?

Yes. The “Settled” status remains visible on your credit report for up to 7 years.

3. Can I get a personal loan after settlement?

Yes, after 18–24 months of clean record and a score above 680.

4. How can I remove the “settled” remark?

Only by paying the remaining balance and getting the lender to update it as “Closed.”

5. Is it better to wait or repay the balance?

If you can afford it, repay. It converts the tag to “Closed” and boosts your score faster.

6. What if I get rejected again?

Wait 3–6 months, improve your score further, and reapply with fewer inquiries.

Conclusion — Settlement Isn’t the End, It’s a Restart

A loan settlement doesn’t define your financial future — your next 24 EMIs do.

Every timely payment, every disciplined month, and every low-utilization statement rebuilds your credibility.

Banks don’t remember your mistakes forever.

They remember your current pattern.

Rebuild quietly. Prove yourself patiently. And soon, lenders will chase you — not the other way around.